A bit of history

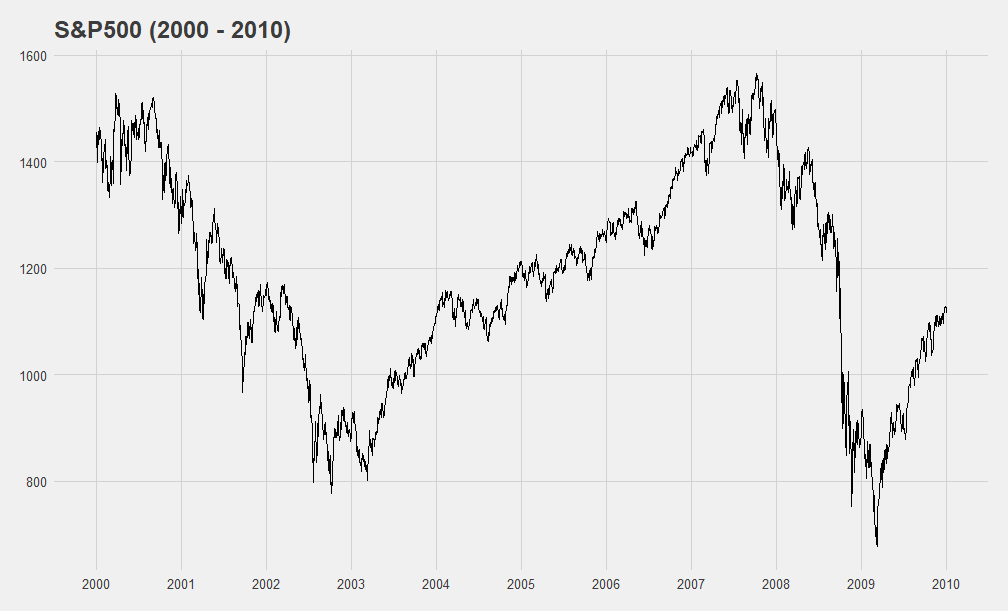

The decade of the 2000s may have been a pretty good decade in many aspects, movies such as the lord of the rings or harry potter were released; music albums such as The Strokes’ “Is this It” or Bob Dylan’s “Modern Times” were released. Nevertheless, this decade was not a good one in economic terms. This decade started with the dotcom crash, which was triggered by the rise and fall of technology stocks. And, this was not the only remarkable economic event of this decade, when the economy seemed to have recovered from this crisis, another crisis broke out, the financial crisis of 2007-2008, triggered by the collapse of the housing market in the U.S. All these economic turbulences can be clearly seen in the evolution of the S&P500 between 2000 and 2010 as shown in Figure 1.

A time of low interest rates

Moreover, these economic disturbances led governments to act severely. Keynesian policies for the activation of the economy began to play a fundamental role. To encourage consumption, interest rates were lowered to near historic lows. Figure 2 displays the US 10 year note bond yield between 1920 and 2020. In this figure, we can see how the dotcom crash pushed down this yield. However, after that it started recovering until July 2007, when the financial crisis started, after that, that yield continued a downward trend.

Stocks as the only attractive investment vehicle

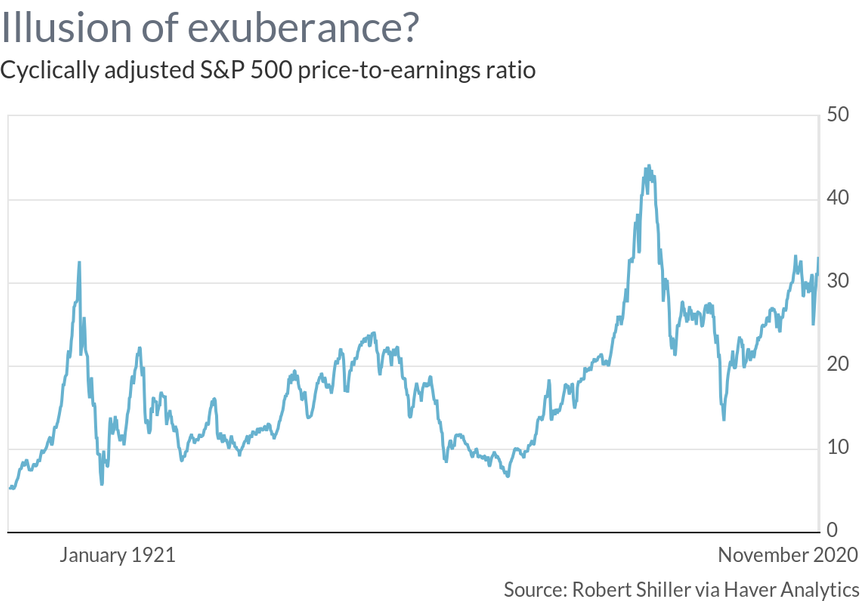

Such a long period of low interest rates inflated stock prices. Figure 3, shows how cyclically adjusted S&P 500 price-to-earnings ratio has been rising during the last decade, being quite high in comparison to other periods of time (specially before the dot-com bubble). Stock prices started trading at a premium, because there were no attractive alternative investments, this channelled much of the liquidity into equities (bonds with almost no interest or even negative interests were not an attractive investment anymore). Moreover, this low interest rate setting has prompted greater investor leverage, due to its low cost. Hence, low interest rates justify high stock prices, since stocks are highly attractive relative to bonds and debt is stimulated due to its reduced cost.

An unexpected event: A global pandemic

2020 was not a good year, this year will always be remembered as the year of the COVID. COVID brought many changes in our lives, which undoubtedly had an impact on the economy. As a result, governments continued to pursue stimulative policies and interest rates remained at very low levels.

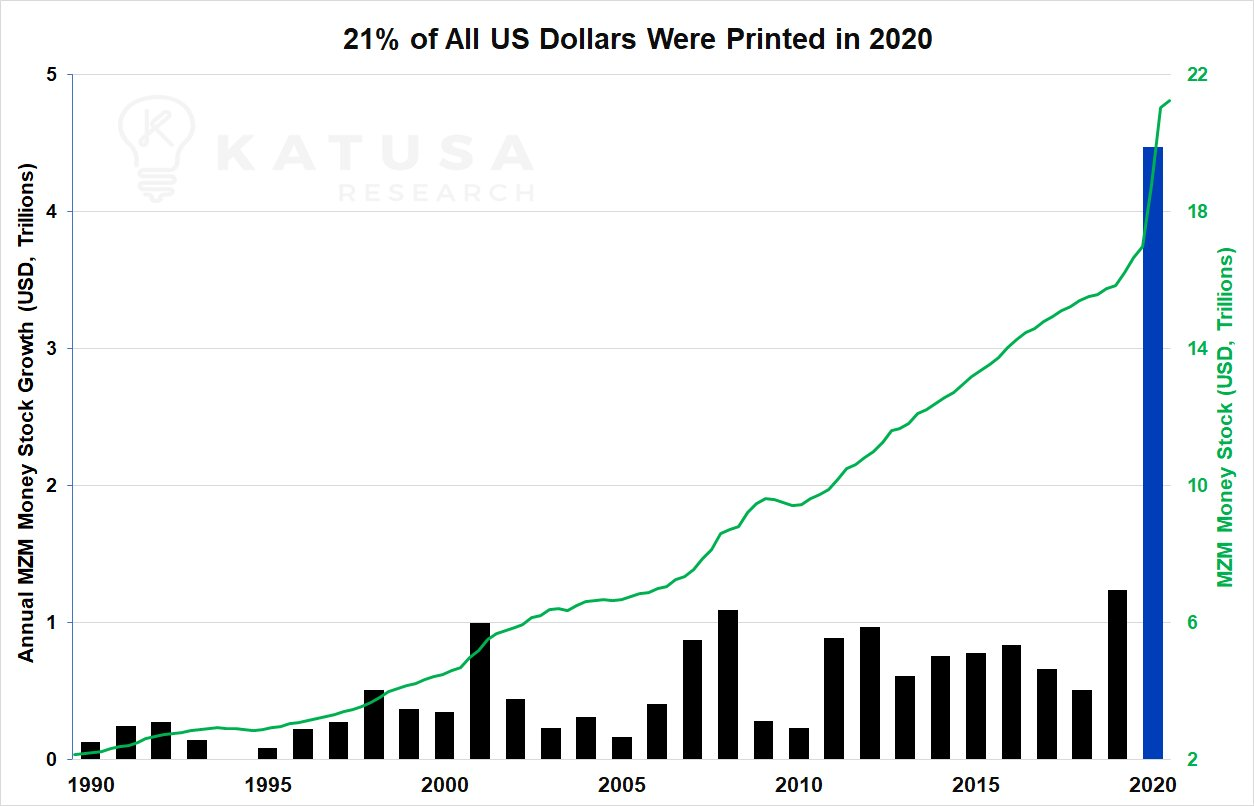

One of the best illustrations of those stimulative policies is the amount of dollars printed in 2020: 21% of the United States dollar was printed in 2020, as shown in Figure 4. This large injection was used for both direct and indirect assistance in the COVID situation. This, at the same time, indirectly channelled part of this aid to the financial markets, increasing their value.

A double-edged sword

Injecting money to the economy is always something controversial. Through the law of supply and demand it is easy to infer that a considerable increase in supply (without a similar increase in demand) will reduce the price of a good. In money, when this happens, we say that the money loses value, i.e. one monetary unit can acquire fewer products. In other words, this is what we call inflation. Even Warren Buffet has shown concern for inflation in the past month:

“We are seeing very substantial inflation […] We are raising prices. People are raising prices to us and it’s being accepted.”

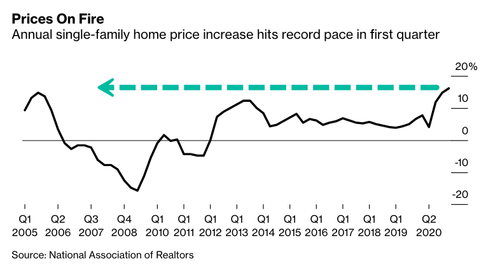

This raise on prices can be already tracked on several indices such as Bloomberg’s agriculture index, shown in Figure 5 and also in the annual single-family home price, as shown in Figure 6.

The appearance of inflation means that interest rates should rise. Something that was already pointed by Janet Yellen at the start of this month:

“It may be that interest rates will have to rise somewhat to make sure that our economy doesn’t overheat”

But what would happen if inflation persists and interest rates have to be risen? Remember that I previously said that stocks are trading at a premium due to the lack of attractive alternative investments. This would no longer be true and this premium would no longer be a thing. In addition, an increase in interest rates would reduce the attractiveness of leverage, thereby encouraging investor’s deleverage. And, thus, we should expect a decrease in the stock price.

The market can not be timed

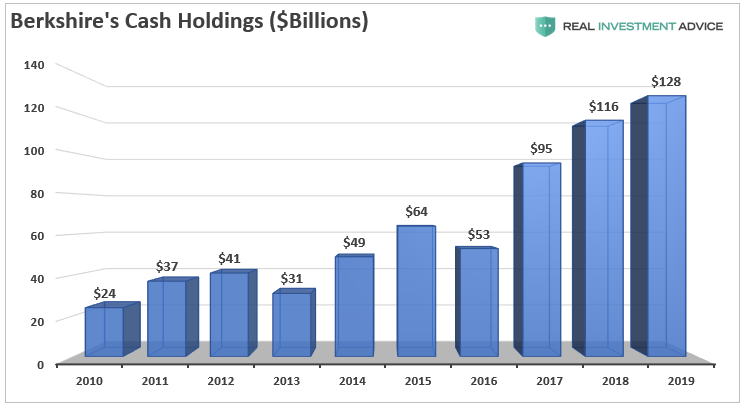

Even with all these indicators, it is difficult to say whether this will happen in the short to medium term. There are many factors which could deter inflation away and interest rates low. As an example, Berkshire Hathaway has been stacking cash during the last years, as shown in Figure 7, playing a slightly more defensive position. This may be due the fact that they already saw that low interest rates during the last decade were driving the stock market at high prices. However, interest rates are still low and during that time the stock market has continued rising.

Summary

- The first decade of the 2000s was characterized by two economic crisis, which defined an economy with very low interest rates

- Low interest rates increased stock market prices, since there were no attractive alternative investments and leverage was cheap. Thus, stock markets traded at a premium.

- The Covid crisis led to a massive injection of money into the economy.

- This money injection is a double-edged sword which may have brought an exuberance illusion awakening a ghost that has been dormant in recent years, inflation.

- The emergence of inflation would imply an increase in interest rates.

- An increase in interest rates would mean that the premium paid for stocks would be lost.

- Despite all these facts, timing the market is no easy task. And thus, other factors could keep inflation away and interest rates away, prolonging this situation.