In recent years, Bitcoin has captured the attention of nearly everyone. Its popularity has surged, driven by both positive and negative events, to the extent that it’s now a rarity to encounter someone unfamiliar with the concept of Bitcoin. However, there remains a somewhat elusive question that many find challenging to address: Can Bitcoin truly be categorized as money? In this blog post, our primary objective is to offer a comprehensive response to this question.

To accomplish this, we embark on a journey to establish a foundational understanding of money: its intrinsic nature, significance, the evolutionary path a commodity must traverse to attain the status of money, the essential attributes it must possess, and an exploration of the various forms of money that have prevailed throughout history.

Subsequently, we delve into a succinct portrayal of Bitcoin, culminating in a decisive exploration of whether it can legitimately lay claim to the title of “money.”

Exchange and money

Barter

Barter is the simplest form of exchange; it refers to the transfer of a good or service for another good or service. For this reason, it is typically considered direct exchange since no third object partakes of the transaction.

Barter requires cooperation between individuals and double coincidence of wants, i.e., that both parties have and are willing to exchange the good or service that the other party desires for the good or service that the other party possesses. Therefore, this form of exchange involves high transaction costs due to the opportunity cost incurred in finding an individual with whom to make the barter.

Indirect exchange and money

These high transaction costs involved in the bartering process led to the emergence and prevalence of indirect exchange, i.e., a type of exchange in which a good or service is exchanged for a more widely acceptable item, which can be subsequently used to exchange for the goods or services desired. Therefore, for indirect exchange to occur, acquired goods must be more marketable than those surrendered. As the greater the marketability of a good, the more it will facilitate the final objective: the acquisition of the desired good or service.

In this way, in indirect exchange systems, the most marketable goods became a media of exchange, i.e., widely accepted. At the same time, as these goods became more widely accepted they further increased their marketability, bolstering their position as a medium of exchange. And, in turn, displaced those goods with lower marketability as means of exchange. Thus, leading to an inevitable scenario in which only a single good was universally employed as a medium of exchange: money.

Functions of money and their development

Therefore, we can define money as a generally accepted medium of exchange. Nonetheless, in several definitions of money, two secondary functions are attributed to it:

- Store of value: It allows to transmit value through time and space.

- Unit of account: It permits the valuation of goods and services.

Notwithstanding, for a good to become money, it is not necessary that it initially fulfills all the above functions. Indeed, goods are converted into money through a process by which they usually acquire some of these functions first, and then others are subsequently developed. In addition, the acquisition of new functions establishes synergies with the previous ones, reinforcing and consolidating their position.

For example, as the practice of using a good as a medium of exchange becomes widespread, people begin to hold it in preference to others, thus developing its function as a store of value and reinforcing its function as a medium of exchange. As a result, acceptability becomes more widespread leading economic agents to set prices using this good as a reference, thereby becoming a unit of account.

On the other hand, for a good whose value is relatively stable, there will be economic agents interested in buying it not to satisfy their most direct needs, but to maintain their future purchasing power. In this way, it will be accepted by a growing number of agents and, therefore, become a medium of exchange. And, thus, economic agents begin to treat it as a unit of account.

Properties of money

Nevertheless, for money to fulfill the above functions, it must meet various characteristic requirements:

- Portability: It must be possible to transport or accumulate a large amount of value in a small amount of space, thereby facilitating transferability and hoarding.

- Divisibility: Money should be divisible into different units to enable precise pricing and facilitate transactions.

- Uniformity: It must be easy to identify units of money having the same value, enabling the counterparty receiving the money to promptly discern its value. Thus, facilitating its transferability.

- Durability: It must remain intact over time without physically degrading or disappearing, therefore favoring its hoarding.

Types of money

This subsection is merely for informational purposes and is not relevant for the understanding of subsequent sections of the post. Readers who wish to omit it, may do so by clicking here.

Throughout history, money has taken many forms. Although today fiat money is the norm, commodity money characterized much of earlier history.

Commodity money

Commodity money refers to real units of a specific commodity universally accepted as a counterpart for goods and services. Accordingly, commodity money has intrinsic value. Historically, a myriad of commodities has served at one time or another as a medium of exchange: animal skins, salt, barley, tea, gold, silver, tobacco, etc.

As economies became more complex, increasing the number of payments, commodity money became cumbersome. The quality of the metals was continually tested to ensure that they had not been tampered with or that they were not of a lower grade than assumed. On the other hand, agricultural products were relatively difficult to transport compared to metals because of their lower unit value. For this reason, two alternatives emerged that sought to solve these problems: coinage and representative money.

Coinage was a revolutionary invention that changed people’s way of thought. Coinage seems to have first occurred in the Kingdom of Lydia around 600 BC when the first electrum coins were minted, a natural alloy of gold and silver. (recent findings suggest that coinage may have originated in China a few years earlier, near Guanzhuang in Henan province). Consequently, metallic coins are a type of commodity money, which is highly transportable and divisible. Moreover, minted coins contained a mark that guaranteed their weight and purity, i.e., their value, thus solving the uniformity problem that untreated metals faced.

Representative money

Representative money is money whose value does not derive from the value of the material it is made of, but from what it represents, since each monetary unit is supposed to represent a fixed quantity of something that has real value.

Some scholars have suggested that this form of money pre-dates coinage. In the ancient empires of Babylon, Egypt, China, and India temples, and palaces were considered inviolable, the former due to religious reasons and the latter due to the heavy protection they possessed. Therefore, they became safe places to store precious goods. Depositors received a certificate attesting deposits, which was a claim to the deposited goods. These certificates have been associated with multiple objects which were used in international trade, such as glazed scarabs in Egypt and cylindrical seals in Babylon and India. For this reason, these certificates are believed to have been used as a means of payment. Furthermore, due to the implementation of the gold standard, representative money occupied a central role during the 20th century.

Fiat money

Fiat money refers to money that has no intrinsic value and does not represent anything of intrinsic value. Public trust in both the issuer and the money itself is what drives its value. Such trust can be attributed, in most cases, to the confidence in the future stability of money’s purchasing power.

Some authors have defined state-issued fiat money more critically as credit reimbursable for the payment of future tax obligations. And, therefore, associating fiat money as a way of using a government’s liabilities as a store of value.

In 1971, following the end of the Bretton Woods agreement, we find the emergence of modern fiat money. Nevertheless, in the fifth century B.C in Carthage, we already find one of the earliest known forms of widespread use of fiat money. This money was a small piece of leather sealed by the state, which enveloped a mysterious substance that nobody knew its composition except the maker. Only by breaking the seal, its composition could be known. However, in the presence of this event, this money was considered worthless.

Recent studies have speculated that the mysterious substance was, in fact, tin or a compound of copper and tin and that the wrapping of this compound was not leather, but parchment.

Cryptography as a means of privacy and the emergence of bitcoin

In the early ’90s, a movement called cypherpunk emerged. It was a libertarian-minded group that wanted to promote cryptography as a means of consolidating and increasing freedom. Cypherpunks published two documents setting forth their goals and ideals: The Crypto Anarchist Manifesto and A Cypherpunk’s Manifesto. In them, they promoted cryptography to increase privacy and anonymity and decentralized software to make their censorship more difficult.

In 1998 Nick Szabo and Wei Dai independently envisioned how these ideas could be applied to money, referring to them as b-money and Bit gold, respectively. For this purpose, they both envisioned a scheme in which balances were stored in a distributed database, and the creation of money was done through the solution of a problem, whose solution is easy to verify.

In 2008 Satoshi Nakamoto published a paper titled: Bitcoin: A Peer-to-Peer Electronic Cash System. In this paper, Nakamoto combined several previous inventions to create a purely peer-to-peer version of electronic cash.

At the beginning of 2009, Nakamoto started the peer-to-peer network. Moreover, he released the Bitcoin source code and compiled binaries on Sourceforge.

A concise overview of how Bitcoin works

Each time a transaction occurs, the network records the Bitcoin address of the receiver and sender together with the amount transferred. This information is entered into the end of a ledger, called the blockchain. The blockchain is updated about every 10 minutes, and it is sent to every full node (computers connected to the Bitcoin network that verify all of the rules of Bitcoin).

Every transaction is encrypted with public-key cryptography and is verified by miners, computers connected to the Bitcoin network that secure the blockchain. The main objective of the miners is to fix the transaction history and prevent transaction fraud. This is done by solving a computer-intensive process by which individuals involved are rewarded with newly minted Bitcoins.

Moreover, rewards given to miners are not always the same, yet they decline geometrically, with a 50% reduction every 210,000 blocks. This pattern was established because it approximates the rate at which gold is extracted.

Is Bitcoin money?

Bitcoin meets all the necessary characteristics required to fulfill the functions that we previously stated that money must accomplish. As a digital asset, it is extensively portable, being its transferability and accumulation easy. In addition, it is deeply divisible: one Bitcoin can be divided into 100 million units, commonly known as satoshis. Likewise, the digital nature of Bitcoins makes them uniform and durable.

However, the fact that it meets the necessary characteristics to fulfill the functions of money does not imply that it fulfills them. Consequently, before we can say whether Bitcoin is money or not, we must first analyze whether it fulfills these functions: (1) generally accepted medium of exchange, (2) store of value, and (3) unit of account.

- Generally accepted medium of exchange: As of today, Bitcoin is not a generalized medium of exchange. We cannot go to the bakery next to our house and buy bread with it, nor can we go to a car dealership and buy a car with it.

- Store of value: Bitcoin has historically had severe price volatility, which is not favoring its function as a store of value.

- Unit of account: The limited adoption of Bitcoin as a means of payment and its price volatility do not foster its use as a unit of account.

Thus, we can say that Bitcoin currently cannot be considered money. Notwithstanding this, given the attractive properties of Bitcoin, we might ask ourselves a slightly more complex question: is Bitcoin in the process of becoming money?

Is Bitcoin in the process of becoming money?

In the beginning, Bitcoin had a highly volatile price, as it was a new, virtually unknown asset that very few people owned. Nevertheless, Bitcoin was an asset with quite appealing monetary properties, coupled with a decentralized scheme and a finite money supply.

These properties led more and more economic agents to believe that Bitcoin could become a future store of value and, thus, decided to acquire and hold Bitcoin. Likewise, the growing demand for Bitcoin led to an increase in its popularity, which drove more economic agents to reach this reasoning. This escalating demand not only bolstered Bitcoin’s popularity but also created a self-reinforcing cycle of adoption, occasionally disrupted by external factors.

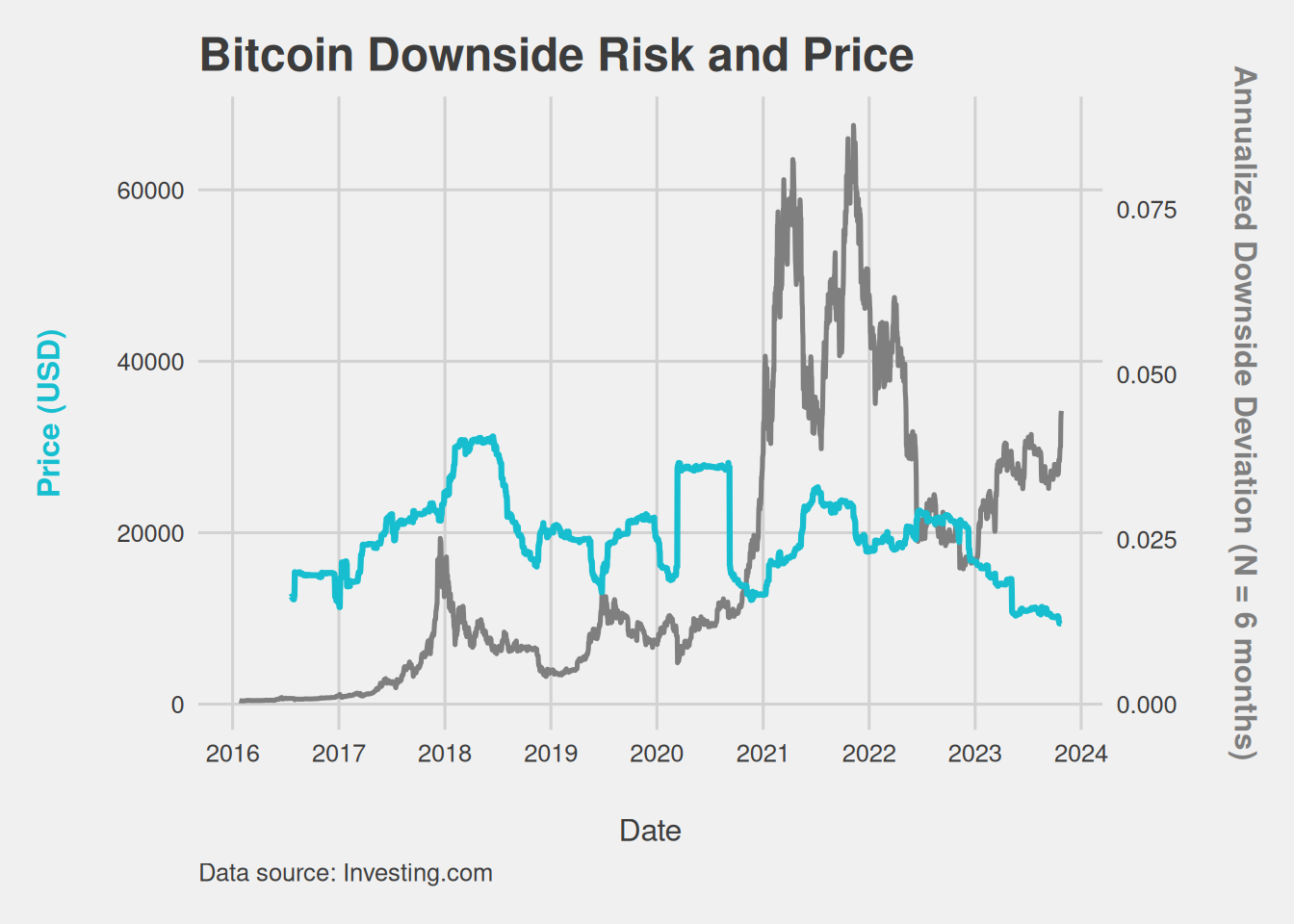

This progression led to a notable reduction in Bitcoin’s downside volatility, as demonstrated in Figure 1, making it increasingly attractive as a potential store of value. Nevertheless, this trajectory was not a continuous one. Instead, it was interrupted at different points by several external shocks. For instance, on February 8, 2021, coinciding with a low downside volatility period, Tesla announced a $1.5 billion Bitcoin. This event elevated Bitcoin’s appeal, indicating to investors that it could be a lucrative investment, thereby driving up its demand and price.

However, in 2022, a series of external negative shocks, such as the TerraUSD stablecoin crash and the FTX collapse, shook investor confidence in the crypto market. This resulted in a decline in the prices of numerous cryptocurrencies, including Bitcoin, increasing its downside variability. However, after this significant price drop, Bitcoin’s value stabilized, suggesting to investors that the impact of these prior external factors might have dissipated. This stabilization restored their confidence, leading to gradual, albeit progressive, price increases and, consequently, one of the lowest levels of downside volatility for Bitcoin.

This newfound stability motivated investors, prompting numerous major companies like Ferrari to announce their willingness to accept Bitcoin as a payment method. Additionally and primarily, steps taken by Blackrock to launch a Bitcoin ETF further intensified demand, subsequently driving up its price.

Consequently, the adoption of Bitcoin as a store of value is becoming more and more widespread. Once a store of value is well established enough, i.e., many agents understand that this asset is a good store of value, they can start to demand it against the sale of their goods.

Despite this, not many companies do offer their goods or services in exchange for Bitcoin. However, if the popularity and the trend towards increased Bitcoin price stability are not affected mid-term, an increasing number of agents will accept Bitcoin as a means of payment.

Finally, if Bitcoin’s function as a medium of exchange were to develop, it would increase its popularity and at the same time solidify its position as a store of value. Enabling future economic agents to start accounting with Bitcoin, i.e., opening the possibility of development to the function of unit of account.

Therefore, we cannot say that Bitcoin is in the process of becoming money, but we can say that Bitcoin is currently in the process of becoming a store of value. That said, whether such a function is widely recognized depends on the maintenance of the trend in which it is now present: further decrease in its downward volatility without giving up its current popularity. Moreover, the development of other functions as a generalized medium of exchange and unit of account is still a long way off and is conditional on the soundness of the development of the store of value function. In addition, even if at some point the store of value function is fully developed, the development of other functions will still remain highly uncertain.

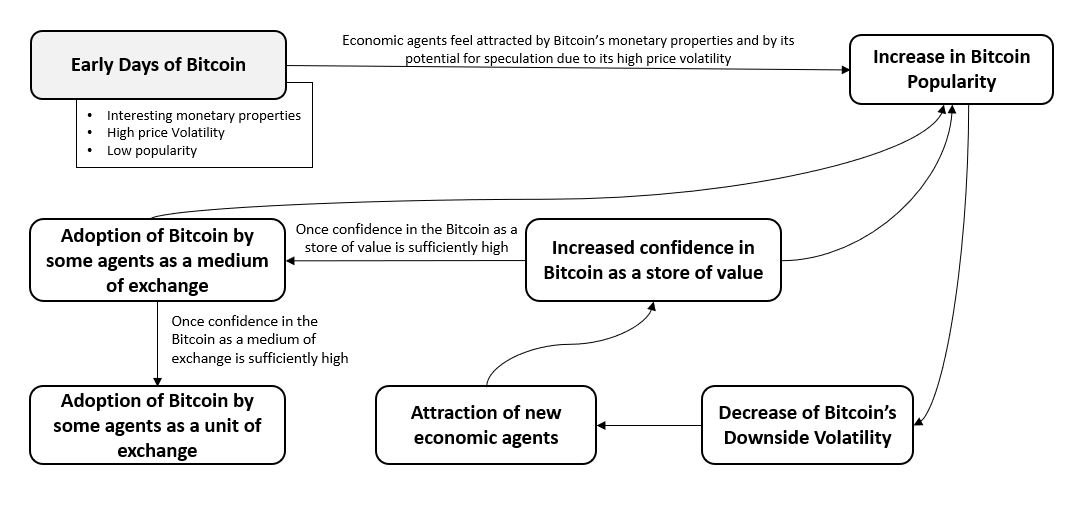

Figure 2 summarizes the process by which Bitcoin could obtain the functions of money and thus become money. Take into account that this figure is an abstraction and does not consider various factors that could influence this process. This includes the potential impact of external shocks, exemplified by the events of 2022, as well as the variable durations of each transition phase. Moreover, it’s essential to acknowledge the non-linear nature of this progression, where steps forward can be accompanied by steps backward, adding complexity to the overall monetization process.

Recently, Taleb has argued that Bitcoin can never be a store of value, since its fundamental value is 0. In the next subsection we address this criticism.

Against Taleb’s argument of Bitcoin’s impossibility to become a store of value

In the summer of 2021, Nassim Taleb published a short article entitled Bitcoin, currencies, and fragility, in which one of his arguments is that the value of Bitcoin is exactly 0 and, therefore, Bitcoin cannot be a store of value.

To argue this, Taleb relies on the premise that the fundamental value of any asset is equal to the sum of the present value of its expected future cash flows together with the terminal value that the asset will have.

Therefore, as Bitcoin does not generate cash flows, i.e., the mere fact of owning Bitcoin as such does not result in monetary payments, meaning that the value of Bitcoin only depends on its terminal value.

Additionally, according to Taleb, Bitcoin is a technology. Therefore, Bitcoin, like any other technology, will eventually be replaced by another. As a result, its terminal value will be 0. Consequently, Taleb argues that since its fundamental value is 0, Bitcoin will not become money.

Nevertheless, in this argument, Taleb avoids two important points: (1) humans are not completely rational, and (2) Bitcoin is in the process of becoming a store of value as we saw in the previous subsection. Taleb may be right, Bitcoin may not yet be a store of value as such. But, this does not imply that it cannot become one, as we have seen in the previous subsection.

The reason behind this is irrationality in the early stages of Bitcoin, at that time it could be valid to say that Bitcoin had a value of 0. Nevertheless, multiple economic agents were attracted by it, which, as we have seen in the previous section, led to the start of the development of Bitcoin’s store of value function. As a result, many economic agents already consider Bitcoin as a store of value, while others expect it to become one in the near future.

Such a fact is critical since assets that act as a store of value provide the holder with a service: the transfer of value in space and time. Consequently, as Bitcoin is in the process of developing its store-of-value function, this implies that the expected flows of Bitcoin are no longer zero, but the implicit value of this service. Therefore, Bitcoin’s fundamental value should be greater than 0.

Therefore, in the case of Bitcoin, we face an instance in which a collective irrationality has endowed this asset with a value that a priori it should not have. Nevertheless, as part of this process, the store of value property has begun to develop, which justifies that this asset has value, and, at the same time, this value allows it to act as a store of value.